Most founders have no idea they can legally pay 0% federal tax when selling their company. Even fewer know that you can still qualify for QSBS (Qualified Small Business Stock) even if you start as an LLC. Here's the clear, founder-friendly guide you wish someone told you sooner.

What Most Founders Miss About QSBS

QSBS is one of the most powerful tax tools available to entrepreneurs. If structured correctly, it can eliminate federal taxes on up to $10 million of gains per founder when you sell your company. Most founders either do not know QSBS exists, think they needed to start as a C-Corp from day one, do not understand the timing rules, or fail to document the key requirements.

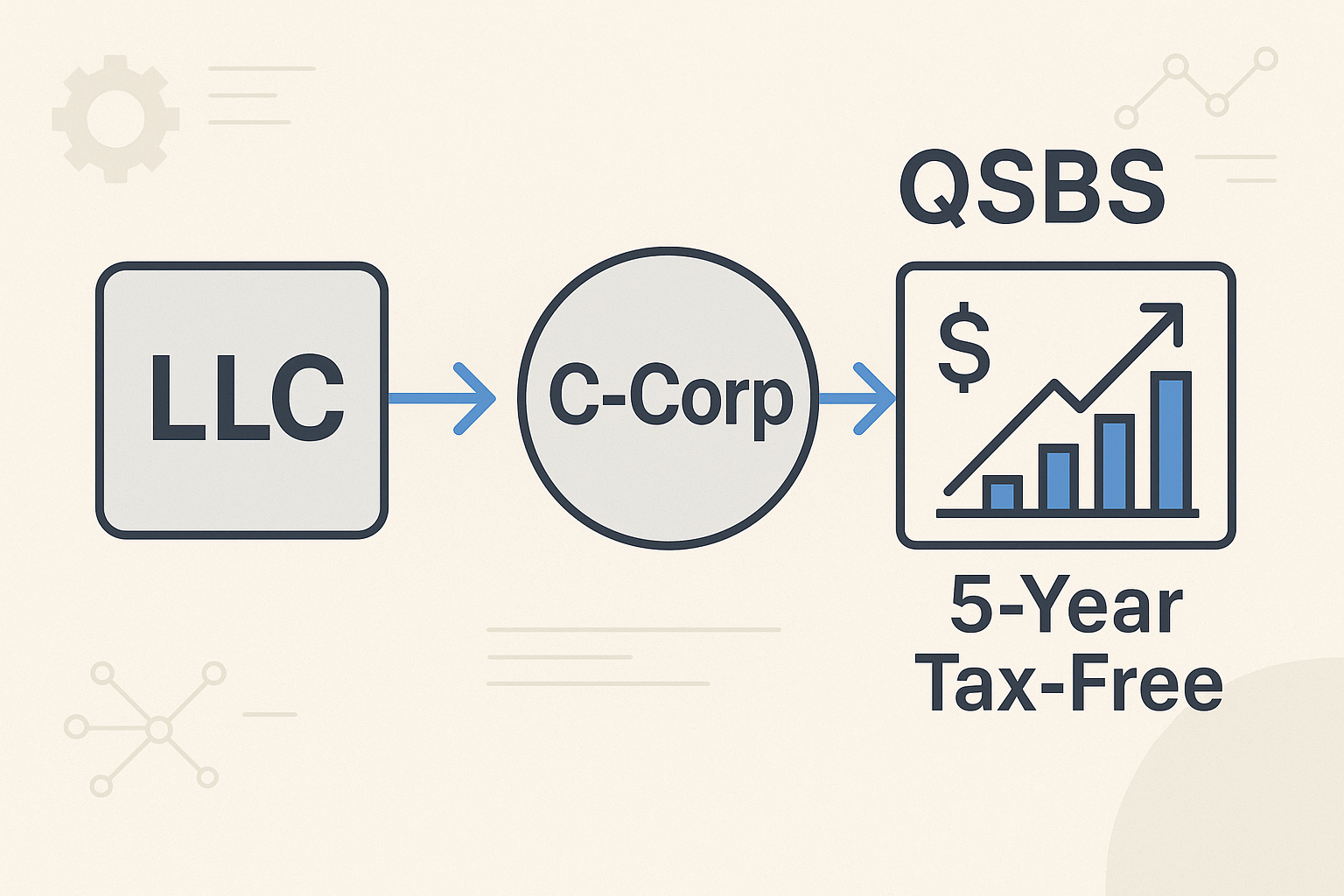

The good news is that you can start as an LLC during the flexible early stage and convert later when the business becomes real, and still qualify.

Why Many Founders Start With an LLC

LLCs give you freedom while you are still figuring out cofounder roles, equity split, contribution value, pricing, strategy, and early customers. You avoid unnecessary overhead and keep full optionality.

Then, once the business has traction, you convert the LLC into a C-Corporation to trigger QSBS eligibility.

What You Must Do to Activate QSBS

The rules are clear and very specific. To qualify for the $10 million tax-free benefit, you must meet the following requirements.

1. Convert to a United States C-Corporation

QSBS only applies to stock issued by a United States C-Corp. You can convert from an LLC using a tax-free transfer under IRC Section 351 if you and your cofounder control the new corporation immediately after the conversion. This involves creating a new C-Corp and transferring all assets, intellectual property, contracts, and operations into the corporation in exchange for founder stock.

2. Ensure the Company's Assets Are Under $50 Million at Conversion

QSBS requires that the corporation be worth less than $50 million at the time shares are issued. Most early-stage businesses meet this requirement with no problem.

3. Receive Stock Directly as an Individual

QSBS only applies if shares are issued directly to individual founders. Do not hold QSBS stock through an LLC, S-Corp, or trust unless it is specifically structured for QSBS. You should personally own the shares in your name.

4. File the 83(b) Election Within 30 Days

If your QSBS stock is subject to vesting, the IRS requires filing an 83(b) election within 30 days of issuance. This locks in long-term capital gains treatment and starts the five-year QSBS clock immediately. The form is mailed to the IRS. Missing the deadline cannot be corrected.

5. Operate a Qualified Active Business

QSBS excludes certain industries such as finance, insurance, hospitality, and professional services. Most modern online businesses qualify, including:

- SaaS

- Direct-to-consumer brands

- Technology-enabled services

- Mobile apps

- Software tools

- Education and training products

6. Hold the Stock for Five Years

The five-year QSBS clock begins on the day founder shares are issued. After five years, up to $10 million (or ten times your basis, whichever is greater) becomes exempt from federal capital gains tax.

7. Maintain Clean Corporate Records

During an acquisition, buyers will request proof that your stock is eligible for QSBS. You will need:

- Articles of Incorporation

- Founder Stock Purchase Agreements

- Stock certificates or digital records

- 83(b) election receipts

- A clean capitalization table

- Board approvals for stock grants

- Financial statements showing asset values

- Documentation confirming that the company operated a qualified active business

How to File What Is Required

During C-Corp Formation

- File Articles of Incorporation

- Create Founder Stock Purchase Agreements

- Issue founder stock

- Record the stock issuance in the company ledger

- Execute intellectual property assignment agreements

Within 30 Days of Stock Issuance

- Mail 83(b) elections to the IRS

- Send a copy to the company for internal records

Ongoing Requirements

- Maintain corporate minutes and resolutions

- Track asset values to confirm they remain under $50 million

- Keep records demonstrating active business operations

Why QSBS Is So Powerful

Here is what happens under QSBS:

- If your exit is $8 million, you pay zero federal tax.

- If your exit is $10 million, you pay zero federal tax.

- If your exit is $15 million, you only pay tax on $5 million.

With two founders, this can become a potential $20 million tax-free outcome.

Case Study: A SaaS Business That Applied QSBS Correctly

Imagine two founders creating a SaaS platform that helps gyms automate membership billing and training programs. They start as an LLC to keep costs low and move quickly. One founder builds the product, and the other founder signs the first ten gym clients using industry relationships.

Once revenue reaches $25,000 per month, they convert to a Delaware C-Corp and receive founder stock. Both founders file their 83(b) elections on time. Over the next five years, the SaaS product grows to 600 gyms nationwide. A fitness technology company acquires them for $11.5 million.

Without QSBS, their combined federal tax bill would have been more than $2 million. With proper structure and five years of stock ownership, both founders pay zero federal capital gains tax on the first $10 million of the exit.

Conclusion

Starting as an LLC gives founders flexibility when everything is still uncertain. Converting to a C-Corp later unlocks the immense tax advantage provided by QSBS. With the correct structure, documentation, and timing, founders can legally eliminate millions of dollars in taxes at exit.

Legal Notice: This content is provided for general educational purposes only and does not constitute legal, tax, accounting, or financial advice. No attorney-client or advisor-client relationship is created by reading this article. Readers should consult their own professional advisors before acting on any information contained here.